If you've ever applied for a business loan, an SBA loan, a commercial real estate loan, or even a basic line of credit, you've met the Personal Financial Statement (SBA Form 413), the document that makes you question every financial decision you've ever made. Not because of what it reveals, but because of how painful it is to fill out.

And if you're a business owner or real estate investor with any degree of complexity to your finances? It gets worse the more complex your finances are.

This isn't another "how to fill out SBA Form 413" tutorial. You can find those anywhere. This is about why the entire process is broken, why it hits business owners and real estate investors hardest, and how Steady Wealth makes PFS generation nearly automatic — as a byproduct of something you should already be doing.

What is a Personal Financial Statement (and why does every bank want one)?

A Personal Financial Statement (commonly called a PFS) is a snapshot of everything you own and everything you owe. Total assets minus total liabilities equals your net worth. Banks use it to evaluate you, the individual, separately from your business.

The standard version is SBA Form 413, required for every SBA 7(a) loan, 504 loan, and disaster loan application. But it's not just the SBA. Virtually every commercial lender has their own version of the same form. If you work with multiple banks (and most serious business owners do), you're filling out slightly different versions of the same document for each one.

Here's what the form covers:

Assets: Cash in banks, savings accounts, retirement accounts, accounts receivable, life insurance cash surrender value, stocks and bonds, real estate (market value), automobiles, personal property, and other assets.

Liabilities: Accounts payable, notes payable, auto loans, installment loans, loans against life insurance, mortgages, unpaid taxes, and other liabilities.

Plus supplemental sections for income sources, contingent liabilities, detailed schedules of every stock holding, every property you own, every note payable, every life insurance policy, and unpaid taxes, each with their own sub-fields.

Then you sign it under penalty of criminal prosecution for false statements.

No pressure, right?

Why the PFS is uniquely painful for business owners and real estate investors

The SBA estimates the form takes 1.5 hours. That might be true if you have a single checking account, one house, and a car payment. For everyone else, that number is a fantasy.

The document scavenger hunt

The form itself isn't that complicated. The agony is in what you have to gather before you can even start filling it out.

For a business owner with any level of complexity, that means logging into (or calling, or pulling paper statements from) a constellation of accounts:

- 3-5 bank accounts (personal checking, savings, business operating, business reserve, money market)

- Brokerage accounts (taxable, Roth IRA, traditional IRA, 401k, SEP-IRA)

- Every mortgage statement (primary residence, investment properties, commercial properties)

- Auto loan statements

- Credit card balances

- Business loan documents

- Life insurance policies (and specifically the cash surrender value, not the face value, a distinction that trips up nearly everyone)

- Property valuations for every piece of real estate you own

For someone with 5 rental properties, 2 businesses, and a normal array of personal accounts, you're pulling together 20-40 documents from different institutions before you've typed a single number. Real estate investors and business owners with complex portfolios feel this pain the most.

You do this over. And over. And over.

This wouldn't be so terrible if it were a one-time event. But a PFS has a shelf life. Most lenders require it to be current within 90 days. Some want 60 days. If your PFS is stale, you're starting over.

And the triggers keep coming:

- New loan application? Fresh PFS.

- Annual loan covenant compliance? Updated PFS.

- Refinancing a property? Updated PFS.

- New line of credit? Fresh PFS.

- Bank just feels like asking? Your loan agreement probably gives them the right to request one whenever they want.

Active real estate investors and serial entrepreneurs can easily find themselves updating their PFS quarterly or more often, and each time it's the same document gathering exercise, the same data entry, the same tedium.

Every bank wants it slightly different

You'd think there would be one standard form. There isn't. The SBA has Form 413. Your local bank has their own template. Your commercial lender has a different one. The information is 95% identical, but the layout is different, the fields are in different places, and you can't just photocopy last month's version and hand it over.

The personal vs. business line is blurry (and that's where mistakes happen)

The most common error on a PFS? Mixing personal and business finances. A PFS is a personal financial statement, so it should only include accounts in your name, not your LLC's operating account or your S-Corp's savings.

But for business owners, the line between personal and business is blurry by nature. You personally guarantee your business loans. Your rental properties might be in an LLC you own 100%. Your business checking account might be the one that pays your mortgage. Figuring out what goes where (and only reporting your proportional ownership share of jointly-held assets) is a recurring source of confusion and errors.

The stakes are real

This isn't a casual form. You sign under penalty of criminal prosecution for misrepresentation. Getting a property value wrong isn't just embarrassing. It can delay your loan, kill your application, or worse.

And lenders will check. They'll cross-reference your stated real estate values against public records. They'll compare your income figures against your tax returns. Discrepancies don't just slow things down; they erode credibility with the lender you're trying to impress.

The real problem: your financial data is scattered

Step back from the form for a moment. The PFS itself is just a summary. The real problem is that your financial data lives in 15 different places and there's no single source of truth.

Your checking account balance is at Chase. Your mortgage payoff is at your servicer's portal. Your retirement accounts are at Fidelity and Schwab. Your rental property values are a guess you update in your head. Your business equity is... somewhere between your last tax return and your gut feeling.

Every time you need a PFS, you're reconstructing your entire financial picture from scratch. That's the broken part.

What if your PFS basically filled itself out?

Here's the key point: if you're already tracking your net worth with categorized accounts, you already have 80-90% of what a PFS needs.

Think about it. A net worth tracker already knows:

| What you're tracking | What the PFS needs |

|---|---|

| Bank account balances | Cash on Hand & in Banks |

| Investment account balances | Stocks and Bonds |

| Retirement account balances | IRA / Retirement Accounts |

| Real estate values | Real Estate (present market value) |

| Car values | Automobiles |

| Business equity estimates | Other Assets |

| Mortgage balances | Mortgages on Real Estate |

| Auto loan balances | Installment Account (Auto) |

| Student loan balances | Installment Account (Other) |

| Credit card balances | Other Liabilities |

| Business debt | Notes Payable |

The mapping is almost 1:1. The only things a net worth tracker doesn't typically capture (but the PFS requires) are supplemental details like your mailing address, annual income figures, contingent liabilities, life insurance specifics, and the granular per-property details (purchase date, mortgage holder name, account numbers).

That's the 10-20% you fill in once. The other 80-90%? It's just your net worth data, reorganized into SBA format.

How Steady Wealth's PFS generator works

I built this feature because the problem is obvious if you've ever applied for a commercial loan: you're already tracking all this data for your net worth, so why are you re-entering it on a separate form every time a bank asks?

The PFS is a natural output of the data you're already maintaining. Here's how it works:

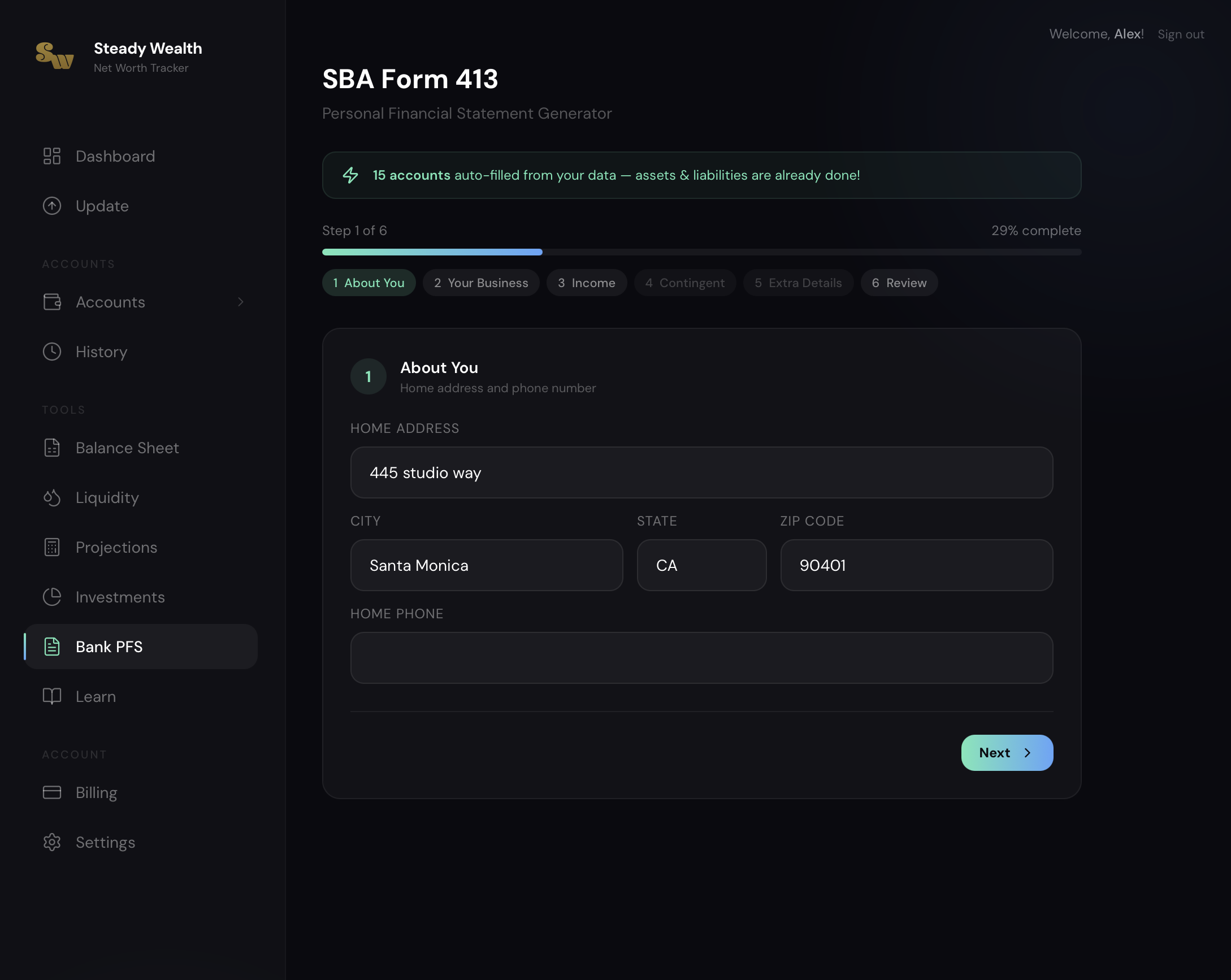

Step 1: Your accounts are already there

If you're using Steady Wealth to track your net worth, you've already categorized your accounts: checking, savings, investments, retirement, real estate, vehicles, mortgages, auto loans, credit cards, business debt. Each one maps directly to a line item on SBA Form 413.

When you open the PFS generator, your assets and liabilities are already populated. You'll see exactly how many accounts are feeding each line item and what the current values are.

Step 2: Fill in the supplemental details (once)

A short wizard walks you through the pieces a net worth tracker can't know:

- About You: Name, address, phone number

- Your Business: Business name, address, entity type

- Income: Annual salary, investment income, real estate income

- Contingent Liabilities: Co-signed loans, legal claims, tax provisions

- Extra Details: Life insurance specifics, cash on hand, accounts receivable

This takes 5-10 minutes the first time. After that, it's saved. You only update what's changed.

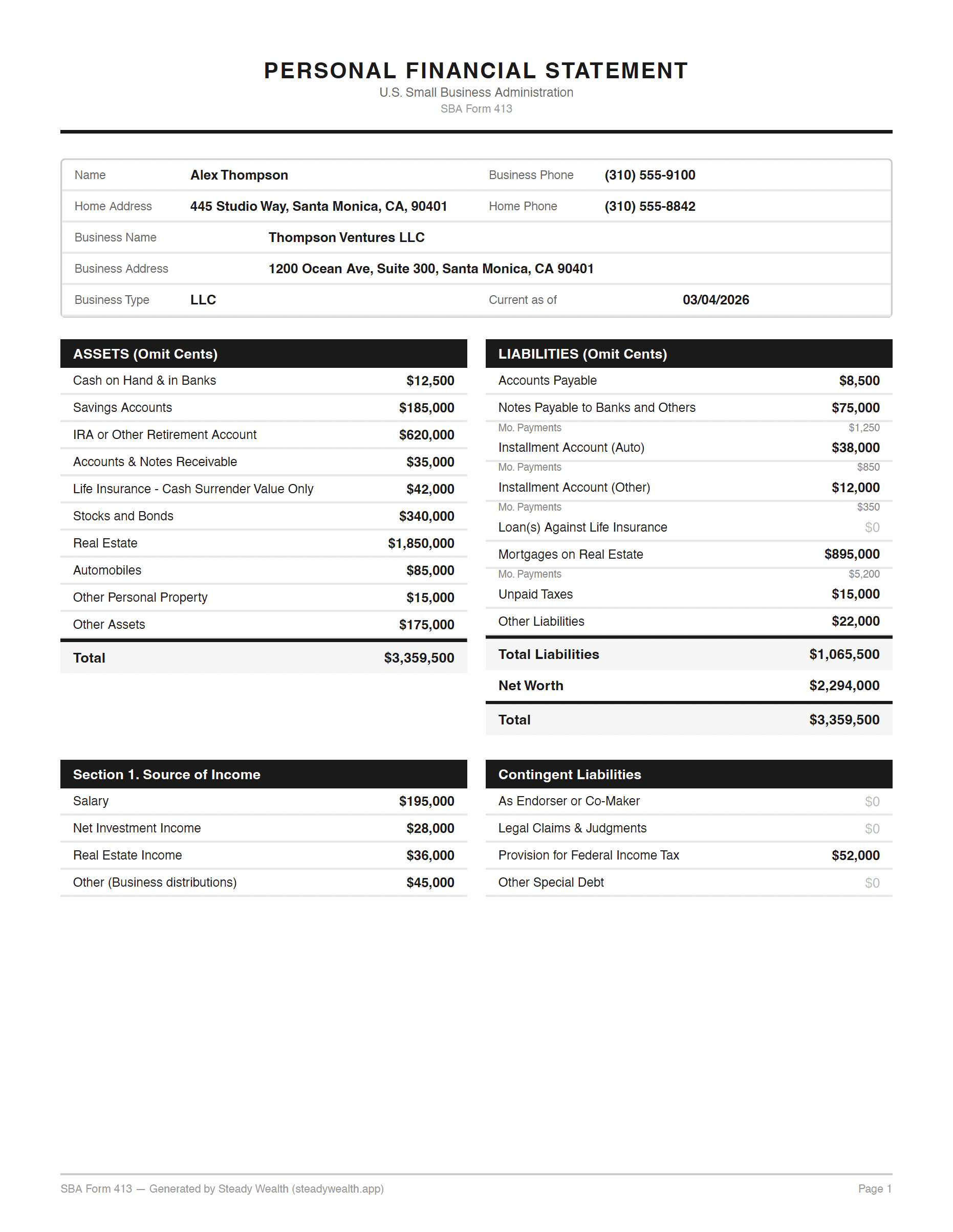

Step 3: Review and generate

The review screen shows your complete Personal Financial Statement: every asset line, every liability line, net worth calculated, income and contingent liabilities included. You can see which accounts contribute to each line item.

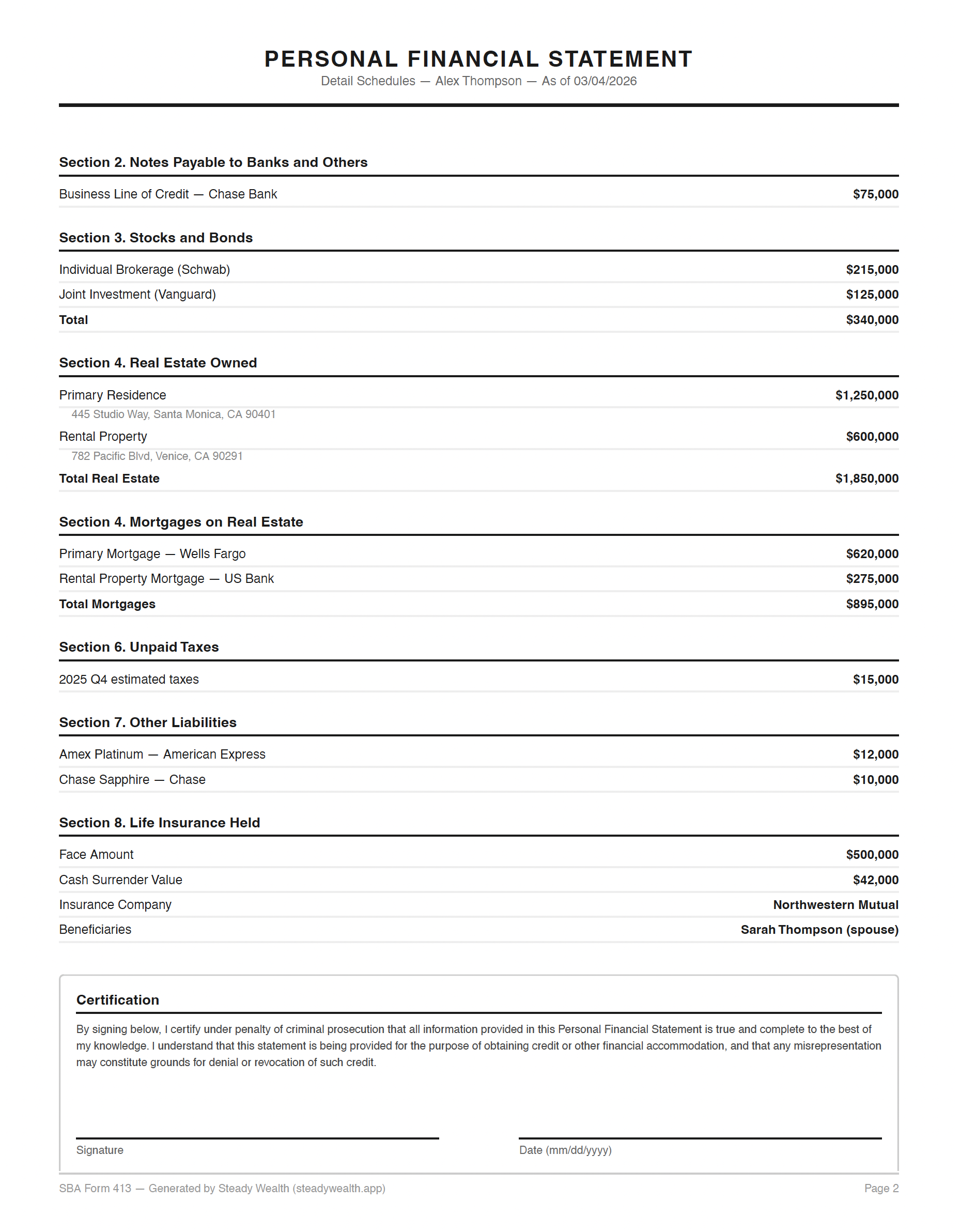

Hit generate, and you get a bank-ready PDF formatted to match SBA Form 413, complete with the detail schedules (stocks/bonds, real estate owned, notes payable, life insurance, unpaid taxes) and a signature block.

Step 4: Next time? Just generate.

Here's where it gets good. The next time a bank asks for your PFS, whether it's 3 months or 3 days from now, you:

- Update your account balances (which you're probably already doing to track your net worth)

- Open the PFS generator

- Hit generate

That's it. Your supplemental details are already saved. Your account balances are already current. The PDF is ready in seconds.

No document scavenger hunt. No logging into 15 different portals. No re-entering the same numbers into a different bank's template. Just generate and send.

Why this matters for business owners

The virtuous cycle

Most people treat the PFS as a standalone chore, something they suffer through when a bank demands it and then forget about until the next time. The data goes stale immediately.

When your PFS is a byproduct of your net worth tracking, something interesting happens: you have a reason to keep your financial data current beyond just personal curiosity.

You know that at some point (next month, next quarter, whenever the next opportunity comes) a lender is going to ask for a PFS. And when they do, you want to be ready in minutes, not days. That knowledge alone is enough to keep you updating your accounts regularly.

It's a virtuous cycle: track your net worth, PFS is always ready, opportunities don't wait on paperwork, you keep tracking because the value is obvious.

Speed is a competitive advantage

In commercial real estate, deals move fast. The investor who can get their loan package to the lender first often wins. When your PFS is always current and generates in seconds, you're not the borrower asking for "a few days to pull my documents together." You're the one who sends a bank-ready PDF within the hour.

Accuracy goes up, stress goes down

When your PFS pulls directly from account balances you're already maintaining, the numbers are consistent by default. You're not guessing what your checking account balance was or estimating your mortgage payoff. The same values you see on your net worth dashboard are the values on your PFS.

And because you're not rushing through a manual process under deadline pressure, you're less likely to make the common mistakes: accidentally including business accounts in personal cash, using life insurance face value instead of cash surrender value, or overstating property values.

One source of truth, any format

Even though different banks use different PFS templates, the underlying data is the same. When your financial data lives in one place with proper categorization, reformatting it for a specific lender's template becomes trivial. Today it generates SBA Form 413 format. The data can power any format.

Who this is for

The PFS generator isn't for everyone. If you have a single W-2 job, one house, and a savings account, you can fill out a PFS in 20 minutes and this isn't your biggest problem.

This is for:

- Small business owners applying for SBA loans, lines of credit, or equipment financing who are tired of the document shuffle every time

- Real estate investors with multiple properties who dread the Schedule of Real Estate Owned section and need to produce updated PFS forms quarterly or more

- Multi-entity entrepreneurs who maintain several businesses and need to carefully separate personal from business finances on their statement

- Anyone with complex finances who has been burned by stale PFS data costing them time or credibility with a lender

If you've ever thought "I just filled this out three months ago and now I have to do it all over again," this was built for you.

Getting started

The PFS generator is available on Steady Wealth's Pro plan. Here's the fastest path to a bank-ready Personal Financial Statement:

- Add your accounts. Set up your assets and liabilities by category. Real estate, bank accounts, investments, retirement, vehicles on the asset side. Mortgages, auto loans, credit cards, business debt on the liability side.

- Enter current balances. Update your account values with a snapshot.

- Open the PFS generator. Navigate to Bank PFS in the Tools section.

- Complete the supplemental details. 5-10 minutes, one time.

- Generate your PDF. Bank-ready SBA Form 413, instantly.

From that point forward, keeping your PFS current is as simple as keeping your net worth current. Update your balances, hit generate. That's the whole process.

Ready to see your full financial picture?

Try Pro free for 30 days. No bank login required. No credit card.

Create your free dashboardFrequently asked questions about Personal Financial Statements

What is a Personal Financial Statement (PFS)?

A Personal Financial Statement is a document that summarizes an individual's assets, liabilities, income, and net worth at a specific point in time. It's most commonly required by banks and lenders when evaluating loan applications. The standard version used for SBA loans is Form 413, but most commercial lenders have their own templates requesting substantially the same information.

When do I need a Personal Financial Statement?

You'll need a PFS when applying for an SBA loan (7(a), 504, or disaster loans), a commercial real estate loan, a business line of credit, equipment financing, or any loan that requires a personal guarantee. Existing loans typically require an updated PFS annually for covenant compliance. Some lenders can request an update at any time per your loan agreement.

How often do I need to update my PFS?

Most lenders require a PFS dated within 90 days of your application. For existing loans, annual updates are standard. Active real estate investors and business owners with multiple lending relationships may need to produce updated statements quarterly or more frequently. The SBA recommends maintaining a current statement at all times.

What's the difference between life insurance face value and cash surrender value on a PFS?

This is one of the most common PFS mistakes. Face value is the death benefit, the amount paid out when you die. Cash surrender value is what you'd receive if you canceled the policy today. The PFS only asks for cash surrender value. Term life policies have zero cash surrender value and should not be listed as an asset. Only whole life and universal life policies have cash value.

Should I include my business bank accounts on my Personal Financial Statement?

No. A PFS covers personal finances only. Business accounts held in the name of an LLC, corporation, or other entity should not be included in your personal cash balances. However, your ownership interest in those businesses is listed as an asset under "Other Assets." This is one of the most common errors on PFS forms and can raise red flags with lenders.

Can I use the same PFS for different banks?

The underlying data is the same, but different lenders often use different templates and formats. While some will accept an SBA Form 413, many prefer their own proprietary form. Having your data organized and current means you can quickly adapt it to any format, even if the specific template varies between lenders.

How does Steady Wealth auto-populate my PFS?

When you track your accounts in Steady Wealth, each account is assigned a category (checking, real estate, mortgage, etc.) that maps directly to a line item on SBA Form 413. When you open the PFS generator, your current account balances automatically fill in the corresponding asset and liability fields. You only need to manually enter supplemental information (address, income, contingent liabilities, life insurance details), and that data is saved for future use.

Is the generated PDF accepted by banks?

The PDF is formatted to match the structure and content of SBA Form 413, the industry standard. It includes all required sections: the asset/liability summary, income and contingent liabilities, and detail schedules for stocks, real estate, notes payable, life insurance, and unpaid taxes. It includes a signature block for you to sign before submitting. While individual lenders may have specific template requirements, the SBA Form 413 format is widely recognized and accepted.